Riley: More Providence Pension Abuse of Public Employees

Tuesday, October 25, 2016

I have been closely following the travails of the Providence Pension system since the fall of 2013 when I completed Graduate work at Stanford University. It was then I noticed the unusual accounting that was peculiar to Providence where 25% of the pension assets earned no return and was described as “other." I could find no other city in the US where “other” accounted for more than .5% of Stated Pension Assets.

Asset Overstatement

Because of this discovery, I began an independent investigation. I asked Providence officials, Wainwright Investment Counsel LLC and the state's auditor what was going on here. I wrote about the process. The story can be reviewed on old columns of mine on GoLocalProv.com or here.

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTThen in 2015 Segal, the new actuary/auditor for the retirement system agreed with my contention that over-stated assets in the pension plan of $63 million dollars was improper and as a result added approximately the same amount to the City of Providence unfunded liability. Whoops! That $60 million dollar bill increased the burden on taxpayers for generations and properly accounted for unwinding a political lie on the books of Providence.

Now more misleading rip-off of employees

The cost of the “asset lie” will start hitting taxpayers in 2018 when the actuary recalculates the funding plan. Alas this is not the only misleading behavior of Providence that is to the detriment of Public employees and the retirement plan.

For decades Providence Fire and Police have been contributing a portion of each paycheck to their own pension plan that is supposed to be matched by an appropriate contribution from the City. The City contribution is to be a match plus an amortization of unfunded contributions for work already performed the workers but not yet paid by the city. The excuses for not paying run the gamut, but suffice it to say that Mayors and Councils tend to sweep costs under the rug today to get re-elected next year.

Unsurprisingly, this type of fiscal management lead to huge cash flow problems. So somewhere along the way, the city, which had continued to allow the workers to contribute 26 pay checks from July 1 to June 30 the next year (fiscal year end), got even farther behind and instead of depositing the workers’ pay check contributions with the Investment Commission and pension plan advisors for interest and capital appreciation, they just held on to the workers money and likely used it for other things.

How do I know Providence screwed workers?

Wainwright Investment Counsel, the city's advisor, was probably sick of my accusations or poor returns and began publishing the cash flows from the City of Providence. This was an extremely unusual disclosure. The documents show that Providence held on to the workers’ contribution not only all year long (zero inflow to pension plan) but sometimes for 16 months before contributing it to the workers’ retirement plans.

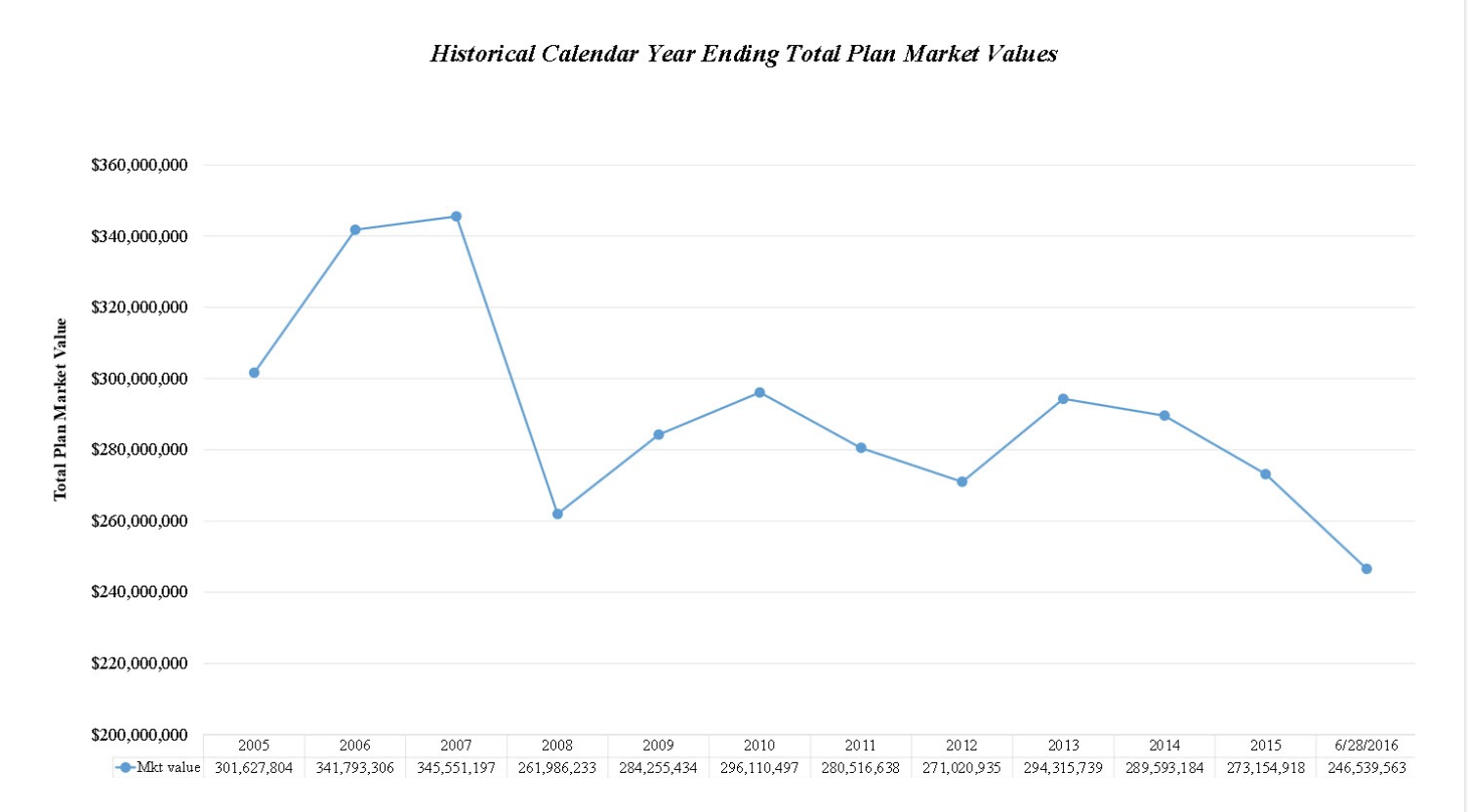

Meanwhile, cash outflows to pay retiree benefits were $8000 a month. Obviously every year the Plan sinks like a stone. If Donald Trump had done that, he would be on fire in Burnside Park and maybe that would have been proper, because really, how low can these Mayors and City Council go? Steal from their own workers? Then bury the next generation in debt?

This report graphically shows a plunging pension plan balance and the negative cash flows since 2005.

So according to Law, when does the employer need to deposit employee contributions in the plan?

ERISA –

If you contribute to your retirement plan through deductions from your paycheck, then the employer must follow certain rules to make sure that it deposits the contributions in a timely manner. The law says that the employer must deposit participant contributions as soon as it is reasonably possible to separate them from the company's assets, but no later than the 15th business day of the month following the payday. For small plans (those with fewer than 100 participants), salary reduction contributions deposited with the plan no later than the 7th business day following withholding by the employer will be considered contributed in compliance with the law. In the Annual Report (Form 5500), the plan administrator is required to include information on whether deposits of contributions were made on a timely basis. For more information, see the Department of Labor's Ten Warnings Signs That Your 401(k) Contributions Are Being Misused for indicators of possible delays in depositing contributions. Source US Department of Labor

Rhode Island Law

Title 45-21 Retirement of Municipal Employees

§ 45-21-38 Receipt of contributions – Investment of funds. – All contributions received by the retirement system from members and participating municipalities shall be paid periodically to the general treasurer and shall be deposited by the treasurer to the credit of the retirement system. All moneys not immediately required for the payment of retirement allowances or other benefits under the provisions of this chapter may be invested by the state investment commission under the provisions of chapter 10 of title 35. The retirement board has full power with respect to the disposition of the proceeds of the investments and of any moneys belonging to the retirement system.

45-21-42

(3)d Notwithstanding any other provisions of the general laws, the payment of the contributions for the employers' share shall be remitted to the retirement board on a monthly basis, payable by the 15th of the following month.

Michael G. Riley is vice chair at Rhode Island Center for Freedom and Prosperity, and is managing member and founder of Coastal Management Group, LLC. Riley has 35 years of experience in the financial industry, having managed divisions of PaineWebber, LETCO, and TD Securities (TD Bank). He has been quoted in Barron’s, Wall Street Transcript, NY Post, and various other print media and also appeared on NBC News, Yahoo TV, and CNBC.

Related Slideshow: Timeline - Rhode Island Pension Reform

GoLocalProv breaks down the sequence of events that have played out during Rhode Island's State Employee Pension Fund reform.

Related Articles

- Riley: Dear SEC, Say Hello to Mayor Elorza & Governor Raimondo

- Riley: Mr. Achorn Do You Still Want Door Number 1?

- Riley: Wainwright Issues Cash Flow Report That Points to Providence Asset Fraud

- Riley: Default, Theft, and Renewed Call for SEC Providence Pension Investigation

- Riley: Puerto Rico and Providence on My Mind

- Riley: A Lively Thought Experiment

- Riley: The Odds That RI Pension Plan will be Fully Funded by 2040

- Riley: Puerto Rican Debt? Treasurer Magaziner Must Fire Cliffwater

- Riley: Why Does NY Have Funded and Honest Pension Plans?

- Riley: Top 10 Signs Providence is Bankrupt

- Riley: RI Treasurer & Hedge Fund Debacle – Worst Returns in a Decade

- Riley: Magaziner Throws Raimondo Under the Bus

- Riley: Magaziner & Elorza Pension Assumptions Ridiculed by Special Master Feinberg

- Riley: A New Low Cost Strategy for Treasurer Magaziner

- Riley: Brexit Slams RI Pension Funds

- Riley: Providence in Big Trouble - Pension Plan Assets Lowest Since 2007

- Riley: Did Smiley Use Bankruptcy Threat to Get Grant, Proving Prov is Lying?

- Riley: Lousy Pension Returns Put One More Nail in Providence Coffin

- Riley: Time to Ditch Hedge Fund Strategy

- Riley: No Need for Commission

- Riley: Elorza - Providence Has Plan to Make Pension Payment on Time

- Riley: RI Pension Shortfall Far Outweighs Budget Surplus

- Riley: Magaziner Drowning in Raimondo’s Hedge Funds Gone Wild

- Riley: Pension Assets Valuation Scam, Elorza Style

- Riley: Close, But No Cigar for Providence