Michael Riley: Rhode Island’s Potential Pension Nightmare

Tuesday, April 15, 2014

Rhode Island’s widely heralded innovation, the Pension Reform Act of 2011, now appears to be in danger, to be tested in court. The trial date set for this lawsuit, affecting state employee pension plans, is now mid-September 2014. When RIRSA was enacted in 2011, the reforms that took place were estimated to save taxpayers approximately $3 billion.

At that time, Rhode Island was challenging Illinois for the worst funded state pension system in America. We were clearly in the midst of a crisis even though we still hear union advocates say the crisis was “manufactured“ by Gina Raimondo. This argument is pure bunk. Not only is it empirically provable that the high rates used to discount liabilities needed to be much lower to provide an accurate picture of funding levels, those rates will come down further toward 6% as suggested by both Moody’s and GASB rule changes that go into effect in 3 months.

Numbers real and fudged

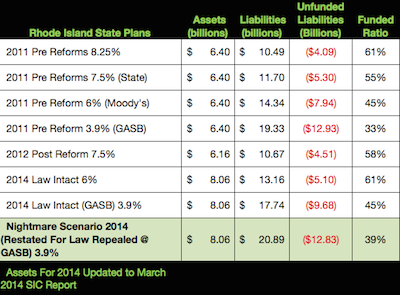

When Rhode Island calculated the actuarial liability in 2011, it was estimated that RI state pension funds were approximately $4 billion underfunded (assets $6.4 billion, liabilities $10.49 billion). Although assets were smoothed and that may no longer be allowed, they were pretty accurate. Liabilities on the other hand, were not accurate and were significantly understated because they were calculated assuming a fully funded plan was going to achieve 8.25% compounded annually going forward. That assumption was wrong for two reasons: the plan was not fully funded (it was 60% funded, assuming 8.25%), and accounting rules are forcing more realistic discount rate assumptions, not Gina Raimondo or Michael Riley as some say.

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTMoody’s will use between 3% and 6% depending on the condition of the plan and GASB rules indicate underfunded plans can no longer just select an investment rate expected return, but must reflect rates consistent with the level of funding. Plans that are underfunded should be calculated using a discount rate of 3.9% (AA 20-year municipal yield).

Gasb 68: The consistency and transparency of the information reported by employers and governmental non-employer contributing entities about pension transactions will be improved by requiring:

The use of a discount rate that considers the availability of the pension plan’s fiduciary net position associated with the pensions of current active and inactive employees and the investment horizon of those resources, rather than utilizing only the long-term expected rate of return regardless of whether the pension plan’s fiduciary net position is projected to be sufficient to make projected benefit payments and is expected to be invested using a strategy to achieve that return

Projected benefit payments are required to be discounted to their actuarial present value using the single rate that reflects (1) a long-term expected rate of return on pension plan investments to the extent that the pension plan’s fiduciary net position is projected to be sufficient to pay benefits and pension plan assets are expected to be invested using a strategy to achieve that return and (2) a tax-exempt, high-quality municipal bond rate to the extent that the conditions for use of the long-term expected rate of return are not met.

The chart below attempts to show a scenario analysis using these accounting rules. It starts by showing our status in 2011, just prior to when reform took place. In 2011, Rhode Island was 61% funded based on actuarial assumptions of a fully funded plan getting 8.25% returns compounded going forward. The reforms including cola suspension and benefit changes had the effect of decreasing the state’s unfunded liability by approximated $3 billion, according to the state figures. At the same time, they changed the discount rate from 8.25% to 7.5%, which increased the projected unfunded liability by over $2.5 billion according to the state.

This chart tries to isolate the impact of the discount rate assumptions both before and post-reform. The key question is this: What are the risks we face individually and as a state if the unions win their lawsuit in court and RIRSA is repealed? I assume that any reform progress at the municipal level dries up and what little progress in municipal pensions proceeds at Commissioner Gallogly’s snail’s pace. Reforms similar to the settlements reached in Providence have very little effect on the unsustainable nature of their plans.

My estimates show the effect of unwinding re-amortization and also the costly effect of returning to the benefit schedules and colas to settings before reform. I used the state’s estimate of $3 billion in savings (now unwound) and added it back to the liability that would be calculated under GASB rules. Because the state fund would still be significantly underfunded even if the law were not repealed, we continue to run the risk of being measured at a 4% discount rate under new rules.

What is the nightmare scenario?

In a nightmare scenario, the existing law would be overturned in the courts and we would then be significantly downgraded by ratings agencies, causing at least 100 times the damage to borrowing costs of not paying Studio 38 bonds. Even if the state then appeals, the $3 billion in savings will be added back to the liability by every rating agency and will be discounted from 3.9% to 4.5%, just like what happened to Chicago a few weeks ago. The state will then be 39% funded, increasing ARCs in both the state and municipalities, thus causing the state’s annual costs to explode beyond the $600 million projected annual cost for 2016. Unwinding RIRSA would immediately increase short-term costs and long-term liability for most cities and towns most of them simply won’t be able to survive.

This scenario would be devastating, and in my opinion would ruin the pension system. The negative effects would harm every taxpayer and destroy the life savings of tens of thousands of public workers past and present. I can’t believe this result is would be good for the next generation of Rhode Islanders. One way or another, the math catches up and the bill comes due. Public employee unions should be careful what they wish for.

Michael G. Riley is vice chair at Rhode Island Center for Freedom and Prosperity, and is managing member and founder of Coastal Management Group, LLC. Riley has 35 years of experience in the financial industry, having managed divisions of PaineWebber, LETCO, and TD Securities (TD Bank). He has been quoted in Barron’s, Wall Street Transcript, NY Post, and various other print media and also appeared on NBC news, Yahoo TV, and CNBC.

Related Slideshow: New England States With the Most State Debt

Related Articles

- Michael Riley: The Harsh Reality of the Pension and OPEB Crisis

- Michael Riley: The Municipal Pension Study Commission Is A Failure

- Michael Riley: Analysing A Crisis

- Michael Riley: The Pension Study Commission Needs To Face Reality

- Michael Riley: Is the RI Pension Commission Making Up Numbers?

- Michael Riley: These RI Cities + Towns Could Be Next in Bankruptcy

- Michael Riley: Moody’s Lowers the Bomb…Look Out Rhode Island

- Michael Riley: West Warwick Is Headed For Disaster

- Michael Riley: Providence Vying for Worst Funded City in America

- Guest MINDSETTER™ Michael Riley: Rhode Island’s Leadership Problem

- Michael Riley: RI Municipal Pension Study Comm. Is in Failure Mode

- PowerPlayer: Republican Congressional Candidate Michael Riley

- Michael Riley: Taveras and Polisena No-Shows at Pension Commission